With interest rates down and the real estate and stock markets declining everyone is trying to figure out how to invest their money to increase their returns. I’ve been scouring the planet looking for opportunities in tax exempt municipals, CDs, and even my life insurance policies. Naturally, some people are looking at income producing properties as a possible alternative – especially since prices are believed to be down.

But how do you evaluate income producing properties? As you might expect there are numerous techniques that might be used. Some people might just look at them in terms of their belief of the underlying value of the building. Does it appear to be fairly valued, given the location, amenities, and condition of the building? However, as someone who has been a stock market investor for decades I tend to look at investment properties in terms of the return I can earn on them and how that compares to other alternatives available to me.

Calculating the Rate of Return

In order to calculate the return on income producing properties one has to first determine their Net Operating Income, which is basically the sum of all sources of income minus the sum of all expenses. For example:

|

Revenue Items |

Expenses |

|

Rent Vending Machines Laundry |

Reserves for major repairs Property taxes Maintenance Management Utilities Legal and accounting fees Insurance Miscellaneous |

Notice that depreciation and mortgage payments are not included as expenses for this analysis. The reason for this is that depreciation is a non-cash expense and mortgage payments are part of the financing decision, not part of the property valuation decision (this is actually the same way you value businesses).

Once you have your Net Operating Income (NOI) you can divide it by your purchase price to begin to get an idea on the return you can expect on your investment. This is known as the Cap Rate, which is short for capitalization rate. If you pay $500,000 for a rental property and your annual NOI is $25,000 then your cap rate is 5%. However, that’s still not the return on your investment. Why not? Because over time you can expect to be able to raise rents and the value of your property should appreciate. For instance, if you can raise rents by 3% per year and if the property can still be sold in the future at the same cap rate at which you bought it then your return will be boosted by 3%. In other words, with a 5% cap rate and a 3% average annual rent increase your total return is now 8%. You can trust me on this or you can contact me to get the mathematical proof, which I would be more than happy to provide.

At this point it’s a good idea to start thinking about how you would finance the deal. If you are going to get a mortgage then you need to compare your mortgage rate to the cap rate on the property. If the cap rate is lower than your mortgage rate then that means that your investment is going to provide a lower return on the money you are borrowing than that money is costing you – in the short run. In other words, you are probably going to end up running negative cash flow in the early years before you can raise the rents sufficiently.

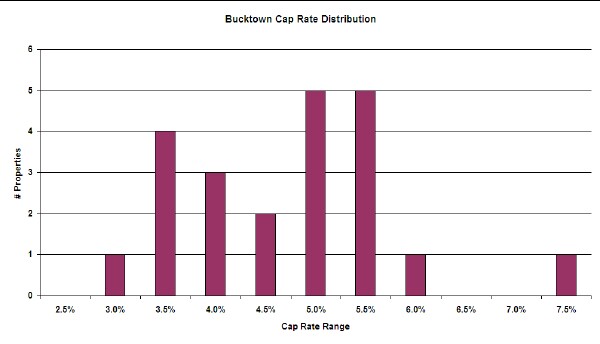

I assume you would probably like to know what cap rates look like in Chicago right now. As I periodically check on cap rates in different Chicago neighborhoods, I’ve decided to share the results I recently came up with for rental properties currently on the market in Bucktown. The chart below shows the distribution of cap rates for 22 rental properties currently on the market in Bucktown:

These rates are estimated based upon very incomplete information from the MLS system so please take them with a large chunk of salt. When determining the cap rates on any property you might be considering you should insist on complete documentation of all sources of revenue and expenses.

At any rate (no pun intended) the cap rates vary between 2.8% and 7.1%. In evaluating possible purchases you would have to ask yourself why the available properties have such differences in cap rates. Perhaps the properties with lower cap rates also have below market rents and you will have the opportunity to raise those rents. Or maybe those properties are just overpriced. Once you have determined the cap rate of a property you can add to it your own assumption regarding annual rent increases.

Tax Benefits

But wait, there’s more! There are also tax benefits in owning rental properties. You can depreciate the portion of the purchase price attributable to the building on your tax return each year so this provides you with annual tax benefits that you need to consider. However, this starts to get complicated and this is where you really need to talk to an accountant because:

- There is this thing called recapture of depreciation when you sell a property that has been depreciated and you will end up giving back some, if not all or more than all, of the tax benefits you took over time. However, there is value in the fact that you had use of the tax savings, interest free, in the meantime.

- There are limits to how much depreciation you can take in any given year if you are not a “real estate professional“.

Do You Want to be a Landlord?

There is just one more thing to consider before investing in income producing property. You need to ask yourself if you really want to be a landlord. When the hot water heater ruptures at 2 AM who are your tenants going to call? Who is going to fix the broken shower head?

And how much is your time worth? Take another look above at the components of your operating expense in the chart above. There is a line for management expense because either you are going to hire someone to do it or you need to consider the value of your time – unless of course you work for free, in which case you should contact me.

Note: If you are thinking about investing in real estate give us a call and we can provide you with information that is more targeted to your particular situation. Also, please keep in mind that all of the above information is not guaranteed to be accurate and before investing in rental properties you should seek the expert advice of an experienced accountant and maybe even an attorney. This post is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. It should not be regarded as an offer to sell or as a solicitation of an offer to buy property.