Well, I guess that’s the problem. They’re up.

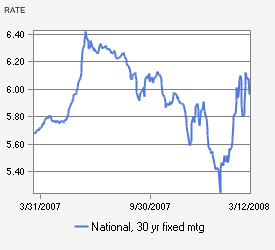

The decline in mortgage rates seems to have not only stopped in the last several weeks but it has actually reversed. During the last 12 months we have seen the rate on 30 year fixed mortgages peak at 6.4% in the middle of last year and then decline to a low of 5.3% in January. However, since then they have bounced back up to 6.1% where they are currently.

If you’ve been listening to the news this may surprise you a bit as you have been hearing a lot about what the Federal Reserve has been doing to help out the credit markets, including lowering interest rates. So you’re probably wondering what is really going on.

If you’ve been listening to the news this may surprise you a bit as you have been hearing a lot about what the Federal Reserve has been doing to help out the credit markets, including lowering interest rates. So you’re probably wondering what is really going on.

The answer is, as usual, that nothing is ever as simple as it seems. First of all when they say that the Federal Reserve is lowering interest rates what they are talking about is the rate on what is called federal funds, which is the rate charged for overnight loans of bank reserves at the Federal Reserve. It’s basically a short term interest rate. However, mortgages are longer term loans and unfortunately as short term rates have moved down investors have become concerned about inflation. Inflation is a byproduct of the abnormally low short term interest rates that the Fed has been creating and when investors become concerned about inflation they want a higher interest rate if their money is going to be tied up for any length of time. So this is one reason that mortgage rates have risen.

But there are other reasons as well. I’m sure you’ve heard about the rising defaults on mortgages. As investors start to get burned by defaults they start to demand a higher interest rate to compensate for those defaults. In addition, with all the turmoil in the financial markets lately large investors have been forced to liquidate some of their portfolios. Consequently they have been forced to sell large quantities of mortgages into the market. With a shortage of buyers in the market, those investors that are buying start to demand a higher rate of return and that also drives up mortgage rates.

So what does all this mean for the average homebuyer and seller? Well, I’m afraid it’s not good news. You can use our loan calculator to experiment with the numbers yourself but according to my calculations an interest rate increase from 5.3% to 6.1% on a 30 year loan results in a 9.1% increase in one’s monthly payment. So either buyers have to buy 9.1% less home or sellers have to cut their prices 9.1%. So, in a way it pays to stay on top of mortgage rates and to be ready to move quickly when rates are attractive. But don’t get carried away. The fact of the matter is that no one can predict which way rates are headed and there is no way to pick the absolute bottom. Besides, there is no guarantee that you will find that perfect home just when mortgage rates bottom out.

For those who are interested, we have created a page on our site to help you stay apprised of the recent mortgage trends.

0 thoughts on “What is up with mortgage rates?”